Chess, like love, like music, has the power to make men happy. This quote by Siegbert Tarrasch is certainly true for the problem below. Solving it, which took me hours, became a moment of joy and beauty.

Thank you, Leonard Barden, who continues to be able to pick interesting problems in his FT column, Many I can solve more or less instantly, or after brief thought. But some prove more challenging, and my habit is to cut them out, and have them with me in my travel bag, for spare moments; or also on my iPad for the same reason.

White to play and mate in 3

Solving this problem took hours, spread over various sessions, with or without the board. I almost gave up, thinking perhaps there was a misprint. I almost put the position into my SmallFish iPad app, but fortunately gave it one more try as the sun went down here in Turkey.

Beautiful, stunningly beautiful, I won’t give the solution in the hope that others can also enjoy Erich Brunner’s 1907 puzzle which Leonard says has stumped solvers for over a century.

Give it a try, it is worth it.

I have recently started reading Chess endings for Club Players by Herman Grooten, published by New in Chess.

Firstly, I dipped into it, to get a “feel” for the book, whether it resonated with me: it did. I have since started reading it from the start, and hope to persevere to the end: a lot of work will be needed to get the most value from it.

I can already tell that the book is (i) a labour of love, by a very knowledgeable endgame player, and (ii) written with the intention of being instructive. These two attributes flow from how he writes. A book written for the reader, not just one more book.

I found his second example (page 11 of his book) extraordinary and fun. Herman had been writing about adjournments, which I remember from my teenage years in the 1970s, and the detailed analyses players did: and the lost role of adjudicator. I adjudicated a fair few games myself (I wonder now whether my judgments would have survived in the engine era). This position was given to Herman’s then coach, you set it for his student: what result?

I analysed it, before reading the solution. The move I wanted to play was 1…Re3, but then 2 Ra7 (2 Rc7 is the same) Rb3 3 b7 and the pawn queens. I looked a bit more, since many years ago I had studied an article by the late Mark Dvortesky on this type of ending, rook+3 pawns on one side of the board, with one side also having a pawn on the other side.

After a while, I saw it! Happy, I turned to the answer, 1…Re3 wasn’t commented on at all, and instead a nice line was given after 1…Rf8, which does indeed draw, elegantly.

But why not 1…Re3? What had I missed? I set up the board and played through my line and then, still puzzled, entered the diagram into my Smallfish iPad app: instantly it pinged that I was right: 1…Re3 does draw. Black can let the pawn promote, because (after 3…Kf8) 4 Ra8+ (if 2 Rc7, then 4 Rc8+ is the same) pushes the king (4…Re7) to a square that it is useful. 5 b8(Q)

5…h5+! 6 gh[] f5+ 7 Kg5[] Rg3 mate!: all Black’s pieces (except the f5 pawn), including the K on e7, take part.

Beautiful!

Pointing out a beautiful line isn’t intended as an adverse comment on the book: in a way, the opposite: there are a lot of beautiful lines in the book, but just as importantly, every page is an opportunity to think for yourself.

I already know I am going love this book and learn a lot from it. Pity it hadn’t been published fifty years ago when some of my games were adjourned.

Since the pandemic, more and more people are required to work from home. This blog post sets out some thoughts on the tax relief which many employees will be able to claim.

In a nutshellFor the current tax year, i.e. from 6th April 2020 to 5th April 2021, employees who are required to work from home are allowed to claim £6 per week as a flat-rate claim, without supporting evidence of expenses actually incurred.

Even "a day" working at home is sufficient to claim £6 per week for the "whole year"I have long known of the weekly Working from home rate: £4 per week until the pandemic struck. I had not given it any attention, though: for most people, a claim of £4, worth 80p for a basic rate taxpayer, is not worth claiming.

And so I initially thought when the government raised the limit to £6 for this tax year alone (we’ll have to see if it is extended). Until my attention was drawn to Martin Lewis’s blog which stated – I still think fairly amazingly- that if a person is required to work at home even for a single day or week, nevertheless he or she can claim the £6 for the whole year. That changed everything, spiking my interest.

£62.40 for a basic rate taxpayer, £140 for a 45% taxpayer, £187.20 for a 60% taxpayerThe claim it for the whole year ‘concession’ means the tax relief is more significant. For basic rate taxpayers, it is worth £62.40; and for 40% or 45% taxpayers even more, and, for instance, for those people in the c £100k-£120k 60% band (the band where £1 of personal allowance is lost for every £2 of income) the saving is £187.20.

To good to be true?Yes, it is, and personally, I don’t think it fits with the wording of the legislation. But I can’t fault Martin Lewis’s diligence in checking and double checking with HMRC, including warning HMRC that he planned to “go viral”. And later I saw this issued by one of tax profession’s professional bodies. And at my suggestion, Clive Gawthorpe of UHY Hacker Young checked with HMRC and published this note. I’m now satisfied that it is appropriate to claim, and am reading it that HMRC are going beyond the strict legislation under the remit given by their care and management powers: in short, it is probably de minimis, and HMRC possibly view it as being more practical to make things easy for all, rather than risk having to police individual claims. Anyway, it is good news.

For further reading, this link to HMRC’s website contains useful information, and I am sure a Google search would result in many hits; and I would also add that this note might be superseded by changes in HMRC policy or further announcements.

How to claim- people who receive tax returnsFor those people who submit a tax return, it may be easiest simply to wait until it is 2020/21 tax return season, and making a claim on the return.

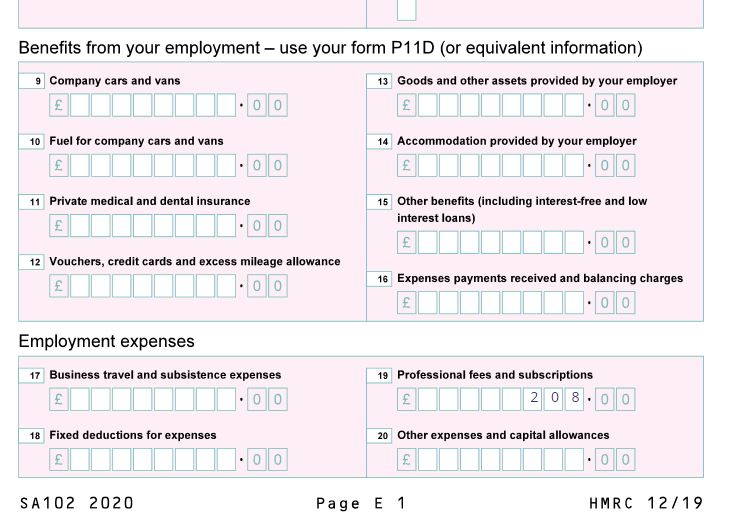

I am not actually sure [I will update when I am] but I suspect simply entering £312 in box 18 of the employment pages will be sufficient.

For the majority of people who don't submit tax returnsNavigate to HMRC’s Working from home site, or use this link.

Answer a few easy yes/no questions, reaching:

Have your National Insurance, payslip, P60 or passport to hand, and create a government gateway account, and then log in on the button. I hope this link works, but if not start with the main ‘are you eligible’ page.

I’m told that if you can apply for a credit card online, or fill in an online form, then you can apply for Working from home relief: HMRC’s system makes it easy. You should then find your PAYE coding is amended.

Other points: complexitiesThis note doesn’t cater for people with multiple employments, or any case other than people employed throughout the year. Consider Rodney, for instance, who retired from employment before Christmas: can he claim £6 * 52, or he is limited to about 9/12 of the relief? I think it would be unfair for Rodney to put 6*52 in box 18 if he files a tax return, but don’t know what HMRC’s systems will do if he uses their online claim service: I suspect the claim will similarly be curtailed when he gets his final payslip.

Other points: 2018/19For 2018/19, the £4 per week can only be claimed for actual weeks which include days at home: that will be some people, including people like my wife, a school teacher: any such people who submit tax returns may therefore want to make a box 18 claim.

A takeaway, lost in the pot, or a lifesaver? Charity donation?Is £62.40 a lot of money? Well, it depends: there will be many taxpayers for whom it is a very welcome boost to their finances, and I hope this blog reaches many, many, such people.

At another extreme, there are many for whom it will just pay for a takeaway, or not noticed, just absorbed into a healthy bank balance. There are some people who would regard it as too small to bother about -for instance, some owners of substantial businesses might decide they haven’t been “required” to work at home, but have done so through choice. I myself have worked from home for six years, and don’t believe it is fair for me to claim, not being “required” because of coronavirus: I won’t be claiming. But my wife, a primary school teacher, has been required at several times since March, and she will claim: but she will then donate all the benefit to charity. Neither of us feel it is right to claim for a full year when she has been in school part of the year; and even for the many weeks she has been working from home, there are people who we would rather give this extra tax relief to rather than keep it ourselves.

I have set up charity donations pages and would encourage anyone for whom the £62 or £140 or whatever sum they receive is a “nice to have” to consider giving either a part, or the whole, to it: because some people are more fortunate than others.

For anyone who would like to donate, the links are:

Allan Beardsworth is fundraising for The Trussell Trust (justgiving.com) (food banks)

Allan Beardsworth is fundraising for Samaritans (justgiving.com) (helping people who are struggling to cope)

Update: one teacher has responded to this blog by donating her tax relief to her school’s breakfast club. That is just as welcome as my two suggested charities: there are so many deserving causes.

And finallyI can’t foresee cases where it is disadvantageous to make a claim, and as I say, Martin Lewis has been diligent in his efforts and others have endorsed it, but this blog is written in the hope it helps others, and readers may wish to take their own professional advice.

Also, I would welcome comments/corrections/updates/experiences.

This note is considered to be correct as at January 2021 when prepared.

In a recent post, I attached my letter to the Chancellor dated 10th April 2020.

I also gave the text of examples. For convenience, a pdf of the examples is below:

Inheritance Tax examples re exemption for front line workers re coronavirus

A few days ago, I posted the text of a letter I have sent to the Chancellor.

Letter to the Chancellor

Attached here is a pdf of the letter itself (with one change, being changing his email address from his Constituency one to his 11 Downing Street one).

Inheritance Tax exemption for front line workers re coronavirus

Examples

I have also now written a few examples of why the exemption might help some front-line workers:

low net assets John, a soldier, dies with an estate below the Inheritance Tax threshold; the present exemption has no effect, not being needed.

married exemption Ann, a paramedic, married to Alan dies with a will leaving her estate to Alan; the present exemption has no effect, not being needed because of the exemption given to legacies to spouses and civil partners.

no valid will Ahmed, a pilot, married to Saadia, dies intestate. Saadia receives part of Ahmed’s estate, and this part attracts exemption. But other parts pass by the rules of intestacy to other family members, and Inheritance Tax would be due, except for the armed forces exemption.

cohabiting siblings Jill, a police sergeant, has always lived with her brother Jack; she owns their home. She died having been attacked at work; her will leaves the house to Jack. Inheritance Tax would have been due, causing Jack to have to sell the house, had it not been for the armed forces exemption.

life insurance not in trust Neil and Lynne live together. Neil, an ambulance driver, dies during the course of attending an accident. Lynne thought that Neil’s estate was too small to be within the charge to Inheritance tax. Alas, like the majority of people (see footnote) the life assurance Neil had taken out was not written in trust and so his estate would have had to pay Inheritance Tax, where it not for the ‘armed forces’ exemption.

living together Frankie and Johnny live together, and felt no need to get married. Frankie, a naval officer, dies in a diving accident. Inheritance Tax would have been payable except for the armed forces exemption.

NHS, Hospice and other front-line workers

There are Ahmeds, Jills, Frankies and Neils in the NHS, at hospices and in other front-line work. It would be a relatively easy amendment to the armed forces exemption- last changed in 2015 to bring in emergency personnel- to exempt them; relieving hardship for a few, and thanking all who day in, day out, put themselves at risk for us.

In summary

The exemption will help very few; it won’t be needed for many. But if it helps a few, or just one person who died trying to help others, isn’t it justified?

One of my hobbies is origami, the art of paper-folding.

I’ve decided to fold NHS blue hearts 💙 and send them on cards to people I know who work at the NHS, in hospices, and in care homes.

It will take time to create the cards, but that is time for reflection and to thank all front-life workers who are doing their best to help people who are poorly with Covid-19 and all the other workload hospitals, hospices and care homes help with. And this is not forgetting GP surgeries, pharmacies, care in the community, bus drivers, binmen, policemen…the people we all rely on without really thinking how important they all are to every one of us.

Folding instructions

Others might like to do the same. Many people will have NHS workers and other front-line workers in their families or amongst their friends. If you would like to fold an origami 💙 for them, I have written folding instructions and they are here:

Good luck, and I hope you enjoy the challenge of folding a 💙 heart (they’re not easy, and if you make one, well done!).

This morning, I wrote to the Chancellor, asking him to give consideration to extending the exemption from Inheritance Tax given to estates of armed services and emergency personnel to NHS, hospice and other front line workers in the fight against coronavirus.

Sadly, doctors, nurses and others have already lost their lives by being exposed to the virus in the course of their work; and more will die, too, before the outbreak is over.

Their estates in the main won’t attract Inheritance Tax; either by virtue of their size, or because of the exemption for bequests to spouses and civil partners. But some estates may trigger Inheritance Tax and could cause hardship. Some will die without having made a will, and thus their estates may pass partly to their spouse, partly to others (attracting Inheritance Tax); others will live as couples without being married or in civil partnerships; and others may be co-habiting siblings.

A sensibly drawn extension of the exemption should be possible: will reduce the financial hardship in some cases, and will be a recognition to all of the debt we owe to all front line workers.

The text of my leter to the Chancellor is pasted below.

10 April, 2020

The Rt Hon Rishi Sunak MP

Chancellor of the Exchequer

11 Downing Street

London SW1A 2AB

By email rishi.sunak.mp@parliament.uk

CEU.enquiries@hmtreasury.gov.uk

Dear Chancellor

Coronoavirus: extension of ‘armed forces’ Inheritance Tax exemption to NHS staff and others

Recommendation: extension of relief

This letter is to suggest that you give consideration to extending the present exemption in s154 Inheritance Tax Act 1984 given to estates of armed forces personnel and emergency personnel to NHS staff and other front-line workers who die when contracting coronavirus in the course of their work.

I have no significant personal interest in the proposal, not being a front-line worker, but consider that it would be a proportionate measure as an additional response to the pandemic. We are all indebted to the risks that such workers expose themselves to each and every day.

My outline proposal is based on the belief that NHS staff and volunteers of all grades, and such staff and volunteers in the nation’s hospices deserve whatever reasonable support the tax code can give them; and that there are many other front-line workers who similarly justify consideration.

I provide further details in the Appendix, including an offer to assist, if needed, in developing the proposals.

Yours faithfully

Allan Beardsworth MA ACA CTA

Appendix: recommendation to the Chancellor to extend the ‘armed forces’ Inheritance Tax exemption to the NHS and other front-line workers. Coronavirus response

Introduction

I am a Chartered Accountant and a Chartered Tax Advisor with over thirty years’ tax experience, principally as a partner in a Big 4 accountancy practice, but since 2015 practising on my own account.

I have no significant personal interest in the proposal. My wife is a primary school teacher but is presently off work due to her pre-existing medical conditions. For completeness, my younger daughter is a medical student; the proposals are not being put forward with a view to any personal gain, but because I think they would in some cases, maybe only a few, relieve hardship inflicted on families and loved ones.

Relief of hardship

A primary benefit of the proposed exemption is to provide a measure of relief from financial hardship.

As with the rest of the population, NHS staff and other front-line workers have a very broad range of financial and relationship circumstances. For those who die with a will bequeathing their estate to their spouse or civil partner, the provisions of s18 IHTA 1984 will lead to no Inheritance Tax.

But, for instance, (i) many people die intestate, so that sometimes not all their assets will be exemption; (ii) many people live as couples, outside a marriage or civil partnership; (iii) others live as co-habiting siblings and are presently not afforded exemption.

Recognition

A secondary benefit of the proposal is to provide a tangible financial benefit to the families of some of the front-line workers who lost their life due to the pandemic.

IHTA 1984, s 154: the existing legislation

There has been a long-standing exemption from Inheritance Tax for the estates of armed forces personnel who die in conflict or as a result of injuries sustained in the line of duty. The original provisions, also in previous death duty taxes referred to wounds inflicted instead of injuries sustained, but extensions in 2015 widened the scope of the relief.

The exemption was broadened following public consultation in 2014 by Finance Act 2015 section 75 to include from 19 March 2014 emergency service personnel and humanitarian aid workers who die in the line of duty. There are now three categories of exemption, listed below, the third being most relevant:

- Death on active service of armed forces personnel;

- Death of police constables or armed forced personnel who are targeted because of their status;

- Death on active service of emergency services personnel; IHTA1984 s153A(1)(a) and (1)(b):

- an injury sustained, accident occurring or disease contracted when that person was responding to emergency circumstances, IHTA84/S153A(1)(a), or

- a disease contracted at some previous time, the death being due to, or hastened by, the aggravation of that disease when the person was responding to emergency circumstances, IHTA84/S153A(1)(b).

IHTA/S153A(6) and (7) have further conditions for emergency services personnel.

(6)“Emergency responder” means—

(a)a person employed, or engaged, in connection with the provision of fire services or fire and rescue services,

(b)a person employed for the purposes of providing, or engaged to provide, search services or rescue services (or both),

(c)a person employed for the purposes of providing, or engaged to provide, medical, ambulance or paramedic services,

(d)a constable or a person employed for police purposes or engaged to provide services for police purposes,

(e)a person employed for the purposes of providing, or engaged to provide, services for the transportation of organs, blood, medical equipment or medical personnel, or

(f)a person employed, or engaged, by the government of a state or territory, an international organisation or a charity in connection with the provision of humanitarian assistance.

(7)For the purposes of subsection (6)—

(a)it is immaterial whether the employment or engagement is paid or unpaid, and

(b)“international organisation” means an organisation of which—

(i)two or more sovereign powers are members, or

(ii)the governments of two or more sovereign powers are members.

Recommendation

I recommend you ask your officials to consider the extension to front-line workers. Since there would need to be boundaries, some thought would be needed, but as a suggestion, a new category of exemption could be introduced for deaths in which covid-19 was cited on death certificates, and in other cases where it was reasonable to assume that the death was due to or hastened by coronavirus.

I presume it will never be known whether a front-line worker contracted coronavirus at work, or on their journey to or from work, or outside of work. Hence my proposal for a “reasonable to assume” clause. HMRC already have experience of determining whether the ‘armed forces’ exemption applies: I would expect cases of difficulty with my proposal to be insignificant.

Linkage could sensibly be made to the Coronavirus Act 2020; for instance, its s1 (3) which stipulates that a reference in the Act to persons infected by coronavirus, however expressed, does not (unless a contrary intention appears) include persons who have been infected but are clear of coronavirus (unless re-infected).

I would be happy to help in any work needed to create a workable proposal; I will send a copy of this letter to my Member of Parliament, Mary Robinson, and to a few other fellow tax professionals and others who I think might be interested and might be able to promote or develop the idea, if it is considered to be a sensible proposal.

Exchequer cost

I presume that the cost to the Exchequer of this measure would be limited. The estates of many deceased front-line workers are likely to be exempt either by size or by s18 IHTA 1984 (spouse and civil partner exemption); the practical effect of the proposals is likely to be limited to the reduction of hardship in a few cases.

cc: Mary Robinson MP, by email mary.robinson.mp@parliament.uk

I’ve decided to call a halt to my daily chess puzzles; the coronavirus pandemic has made me reflect on what’s important and how busy I have been these last too many years, and is causing me to make some changes. The work required to find, write up and post the puzzles has started to outweigh the pleasure of having an audience. Had I been less busy with work and other things I would have continued, but from now on, I will only post on an occasional basis, when I feel I have something interesting to share.

I started this blog many years ago, when I wanted to know how to write a website; and I’ve now done over 3,000 postings.

From now on, my postings will be infrequent,.

Stay safe.

Today’s problem is from the Candidates tournament.

As is my custom, I only say which side is to play: and not giving an idea if the move wins or otherwise, unless on occasion I think signposting would be helpful. Instead, the problems are posed with the instruction to decide what you would play, as in a game.

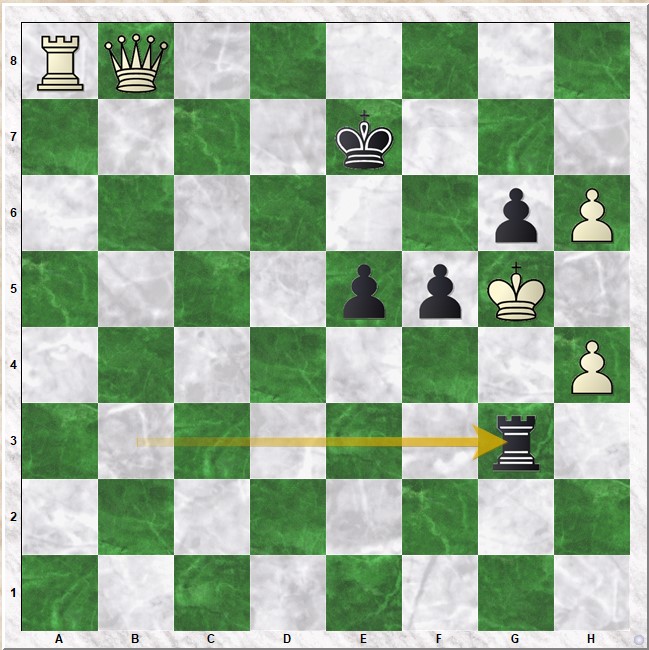

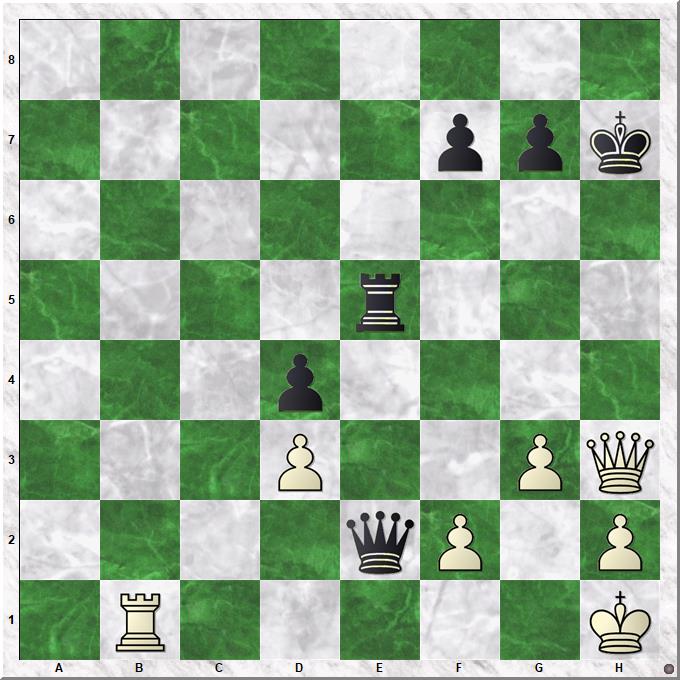

White to play

Nepomniachtchi v Ding FIDE Candidates Tournament, Yekaterinburg, 23/3/2020

Solution

The first move White could play is 1 R6b2, but 1…Qb2! is an easy-to-spot tactic, since the Rb1 is tied to the first rank.

The second move I looked at for White is 1 Rb8, but then the fantastic 1…Re5! holds the balance, due to the back rank mate threat.

White has to play Rd8+ Rh8+! Qc8+ Qh3 wjem je jas a Carlsenesque advanntage:

FEN

3b2k1/5pp1/1RQ5/r7/3p4/3P2Pp/4qP1P/1R5K w – – 0 35

Today’s problem is from the Candidates tournament.

As is my custom, I only say which side is to play: and not giving an idea if the move wins or otherwise, unless on occasion I think signposting would be helpful. Instead, the problems are posed with the instruction to decide what you would play, as in a game.

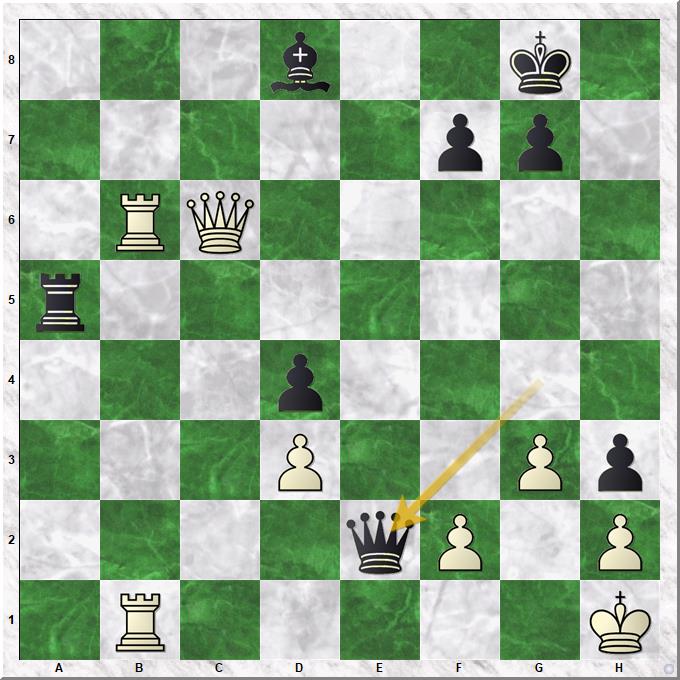

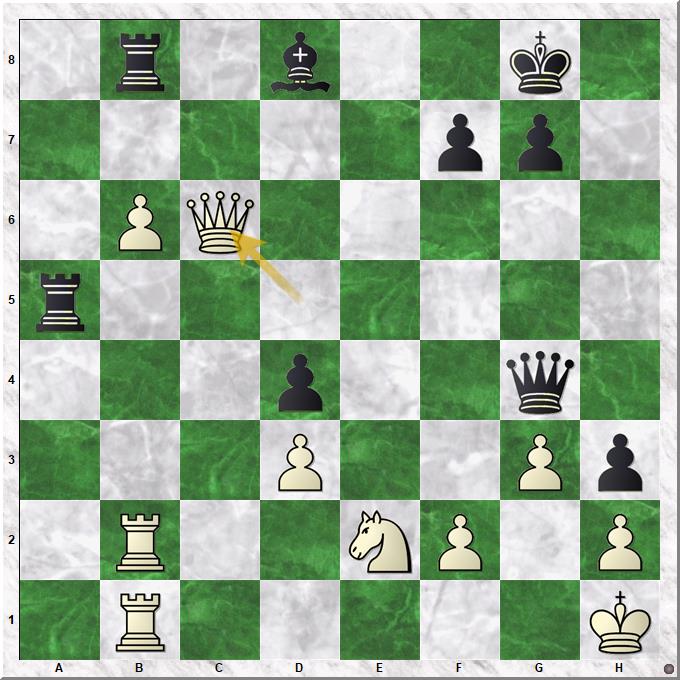

Black to play

Nepomniachtchi v Ding FIDE Candidates Tournament, Yekaterinburg, 23/3/2020

Solution

Black played 1…Rc5 and soon lost, but 1…Rb6! 2 Rb6 Qe2! is equal. I’ll look at why tomorrow.

FEN

1r1b2k1/5pp1/1PQ5/r7/3p2q1/3P2Pp/1R2NP1P/1R5K b – – 0 33